The Rise of Chinese Cars in Europe: Surpassing Mercedes, Overtaking Ford in the First Half of 2025 | BlogMotori.com

The European automotive market is undergoing a profound transformation. Overall registrations have recorded a slight decline, while new players are emerging: Chinese brands. According to JATO Dynamics data, the first half of 2025 marks a turning point, with Chinese brands surpassing Ford and Mercedes.

The European automotive market is undergoing a profound transformation. Overall registrations have recorded a slight decline, while new players are emerging: Chinese brands. According to JATO Dynamics data (source: article “Chinese car brands continue their ascent, outselling Mercedes in June and Ford in H1”), the first half of 2025 marks a turning point, with Chinese brands achieving a market share higher than Ford and managing to surpass Mercedes in the month of June.

In addition to the Chinese advance, two phenomena dominate the scene: the expansion of electric mobility and the structural strengthening of the SUV segment.

The Snapshot of the European Market: Declining Registrations, Growing BEV and PHEV

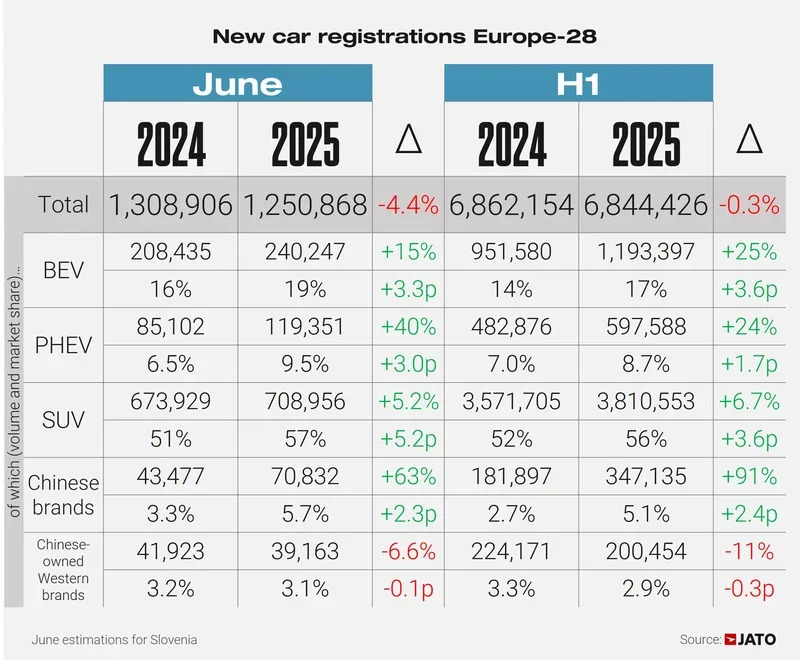

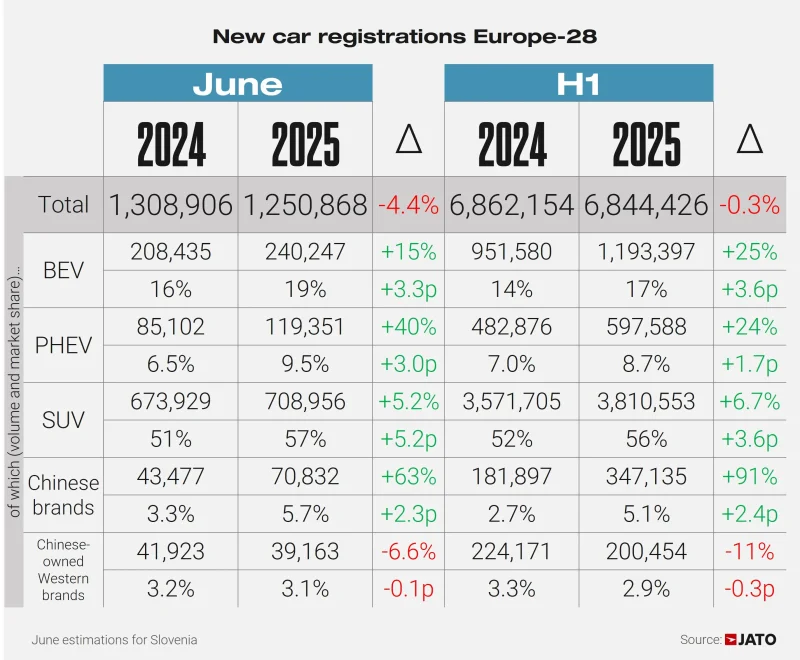

Graph 1 – New car registrations Europe-28

The first graph clearly shows the contrasting dynamics of the sector. In June 2025, total registrations decreased by 4.4% compared to the previous year, confirming the fragility of the market. However, segments with higher technological and sustainable content show signs of vitality:

- BEV (Battery Electric Vehicles): +15% in June and +25% in the first half, reaching a 17% share.

- PHEV (Plug-in Hybrid Electric Vehicles): +40% in June and +24% on a semi-annual basis, with a share close to 9%.

- SUVs: consolidate their dominant position, with a 57% share in June and 56% in the semester.

Chinese Brands Overtaking: Surpassing Ford and Challenging Mercedes

The real surprise comes from Chinese brands, which recorded an increase of 91% in the semester, reaching a 5.1% market share. In parallel, Western brands owned by Chinese companies (like MG or DR) experienced an 11% decline, indicating that consumers are favoring Chinese brands directly rather than their acquisitions of European brands.

The European car market continues to contract, and competition is becoming increasingly fierce. The main beneficiaries are the Chinese manufacturers, who in the first half of 2025 nearly doubled their share compared to 2024, reaching a record 5.1% (+91% in volumes). This result allows them to surpass Ford (3.8%) and closely approach Mercedes (5.2%). In June, overall, Chinese brands even sold more than Mercedes.

Growth is driven by five key players: BYD, Jaecoo, Omoda, Leapmotor, and Xpeng.

-

BYD stands out for its aggressive pricing policy: with over 70,000 registrations in the semester (+311%), it has entered the top 25 of the best-selling brands in Europe, surpassing Suzuki, Mini, and Jeep. The Seal U was among the best-selling plug-ins in Europe, second only to the Volkswagen Tiguan in June.

-

Jaecoo and Omoda (Chery Group) advance mainly thanks to thermal and plug-in hybrid SUVs, such as the Jaecoo 7, the ninth best-selling PHEV in June.

-

Leapmotor recorded over 8,300 units just in June, driven by the city car T03 and the SUV C10.

-

Xpeng establishes itself as the strongest Chinese premium brand in Europe with over 8,300 registrations in the semester, propelled by the SUV G6.

The message is clear: China is not only a player in the European market but is also disrupting historical balances, displacing established brands like Ford and putting pressure on Mercedes.

The Rise of Chinese Brands: From Outsiders to Key Players

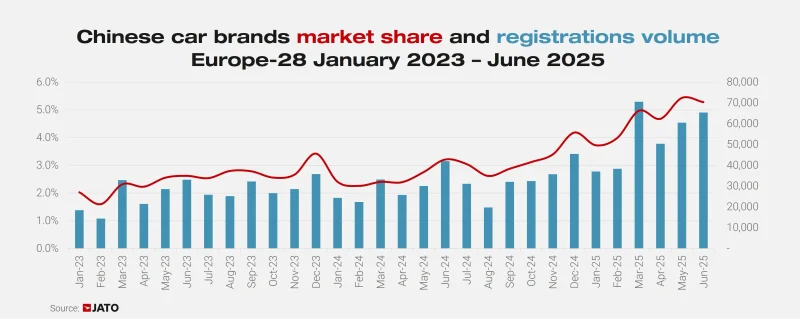

Graph 2 – Chinese car brands market share and registrations volume

The trend of market share and volumes of Chinese brands highlights a steady and progressive growth from 2023 to today, with a significant acceleration during 2024 and the early months of 2025.

- In 2023, their presence was marginal (between 1% and 2%).

- In 2024, the curve began to rise more sharply, surpassing 3% by mid-year.

- In 2025, there is a definitive explosion: share over 5% and monthly volumes exceeding 70,000 units.

The graph also highlights seasonality: peaks are concentrated at the end of the quarter, corresponding with aggressive discount policies and the launch of new models (e.g., BYD Seal U or Leapmotor T03).

The central data is that Chinese cars are no longer a niche phenomenon: their penetration is now structural, with direct impacts on competitive balances in Europe.

The Best-Selling Models: The Strength of the Renault Group and the Advance of SUVs

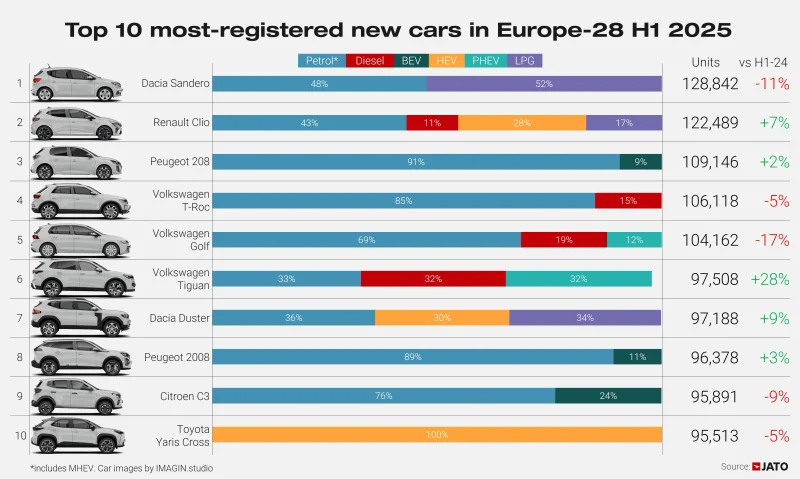

Graph 3 – Top 10 most-registered new cars in Europe-28 H1 2025

The ranking of the ten most registered models in the first half of 2025 reveals interesting trends:

- Dacia Sandero (128,842 units, -11%) maintains leadership despite the decline, indicating that price-sensitive customers remain loyal.

- Renault Clio (+7%) consolidates the role of the French group in popular segments, also thanks to the expansion of the electrified range.

- Peugeot 208 (+2%) remains stable, driven by the electric version.

4-6. Volkswagen T-Roc, Golf, and Tiguan show contrasting dynamics: declines for T-Roc and Golf, strong growth for Tiguan (+28%), highlighting the success of the latest SUVs. - Dacia Duster (+9%) ranks among the bestsellers due to its versatility and competitive positioning.

8-10. Peugeot 2008, Citroën C3, and Toyota Yaris Cross complete the top 10, with the Yaris Cross standing out for its 100% hybrid powertrain, showcasing Toyota's strength in the HEV sector.

The overall picture emphasizes two points:

- The dominance of SUVs: five models in the top 10 belong to this category.

- The resilience of the Renault Group, which occupies the top two positions with Sandero and Clio.

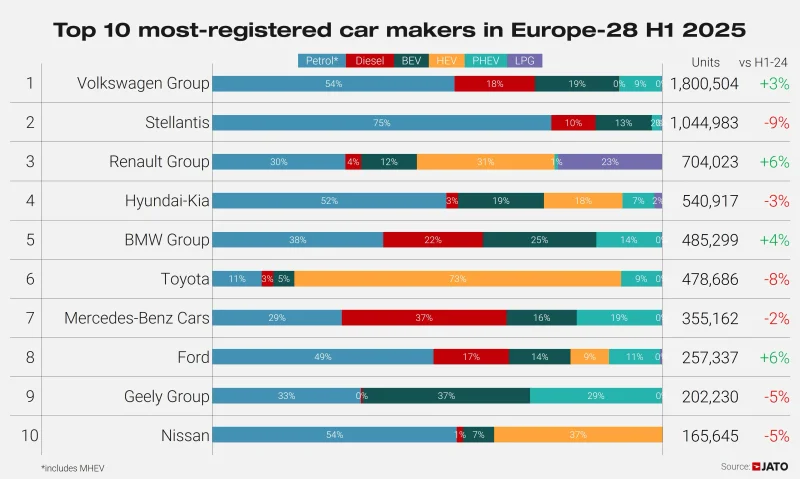

Top 10 Best-Selling Car Brands in Europe in the First Half of 2025

The graph, provided by JATO Dynamics, illustrates the top 10 car manufacturers by number of registrations in the 28 European countries in the first half (H1) of 2025, with a detailed breakdown by fuel type (Petrol*, Diesel, BEV, HEV, PHEV, LPG, and Others) and the percentage comparison with H1 2024. Volkswagen Group dominates the ranking with over 1.8 million units sold (+3%), showing a balanced mix: petrol at 54%, diesel at 18%, BEV at 19%, and PHEV at 9%, reflecting a transition towards electric without abandoning traditional engines. Stellantis follows in second place with about 1.04 million units (-9%), heavily reliant on petrol (75%), with smaller shares for diesel (10%), BEV (13%), and presumably PHEV (2%), highlighting vulnerability to fluctuations in the fossil fuel market. Renault Group is third with 704,023 units (+6%), with a diversified portfolio: HEV at 31%, PHEV at 23%, petrol at 30%, and BEV at 12%, reflecting a hybrid-oriented strategy. Hyundai-Kia (540,917, -3%) and BMW Group (485,299, +4%) show a strong presence in BEV (19% and 25%, respectively), while Toyota (478,686, -8%) stands out for its HEV at 73%, confirming its leadership in hybrids. Mercedes-Benz (355,162, -2%) maintains a high share of diesel (37%) alongside BEV (25%) and PHEV (19%). Ford (257,337, +6%) is balanced on petrol (49%), with growth in BEV (14%). Geely Group (202,230, -5%) is the most focused on BEV (37%) and PHEV (29%), while Nissan (165,645, -5%) relies on petrol (54%) and HEV (37%). Overall, the graph highlights a general growth of electrified vehicles (BEV, HEV, PHEV) among many manufacturers, with a general decline for diesel and a persistent dominance of petrol in some, in a market that sees modest increases for some (like Renault and Ford) and declines for others, influenced by factors such as tariffs, EU regulations, and consumer preferences.

Conclusions: A New Industrial Geography

The joint analysis of data and graphs leads to three fundamental considerations:

- The European market is contracting, but the demand for electrified vehicles continues to grow, albeit at a slower pace than in the past.

- Chinese cars are reshaping the competitive landscape, with shares now comparable to those of major historical brands. Their growth is structural and not a flash in the pan.

- European manufacturers must react, accelerating the offer of accessible and diversified models capable of countering the aggressive pricing and technological variety of Chinese brands.

The year 2025 may be remembered as the year when the European automotive sector definitively lost its monopoly over its domestic market, paving the way for a new industrial geography dominated by global competition and energy transition.